Market Update

2. Juli 2025

Back to negative interest rates in CHF

What does the return to zero rates mean for CHF investors – and which alternatives can still deliver stable returns?

Find out why an active, liquid alpha portfolio makes all the difference now.

< Deutsche Version >

Back to negative interest rates in CHF

A full three years after the interest rate shock of 2022, the Swiss National Bank (SNB) has cut the key interest rate back to 0% and market interest rates at the short end are already negative again. This brings us back to the environment of 2014 - 2021, when the yield curve for CHF bonds was largely negative. Then as now, it made no sense to take risks if you cannot achieve a return. 2022 also clearly demonstrated how painful bond investments can be if interest rates suddenly rise.

The risks are no smaller today than they were then. In addition to another wave of inflation due to US customs policy and de-globalization, the global debt crisis is also coming to a head, which will force interest rates higher. It is not without reason that the US Federal Reserve is very reluctant to cut interest rates so that it is not suddenly forced to do the opposite.

Alternatives to bonds, such as real estate, infrastructure and private debt, are all illiquid. In addition, the expected returns are rather modest when you consider that you are committing yourself for 10 years or more.

In our view, the best risk/return option is a liquid alpha-oriented hedge fund portfolio. A well diversified portfolio across regions, asset class and niche strategies that are uncorrelated with each other is crucial for a steady and stable return.

Our portfolio has achieved a good +5% per year in CHF, net of all fees, over 10 years since 2015, while interest rates have been negative almost continuously. As all investment strategies are largely market-neutral and the managers are proven specialists in their niches - with long, first-class track records that have overcome many crises - a similar result is very likely to be achieved over the next 10 years. +5% per annum or 0% per annum makes a huge difference over 10 years, which would make life easier for many pensioners.

The chart above shows that the Liquid Alpha Portfolio in CHF has always performed positively regardless of the market environment, while neither Swiss Confederation bonds nor corporate bonds with good credit ratings in CHF have earned anything.

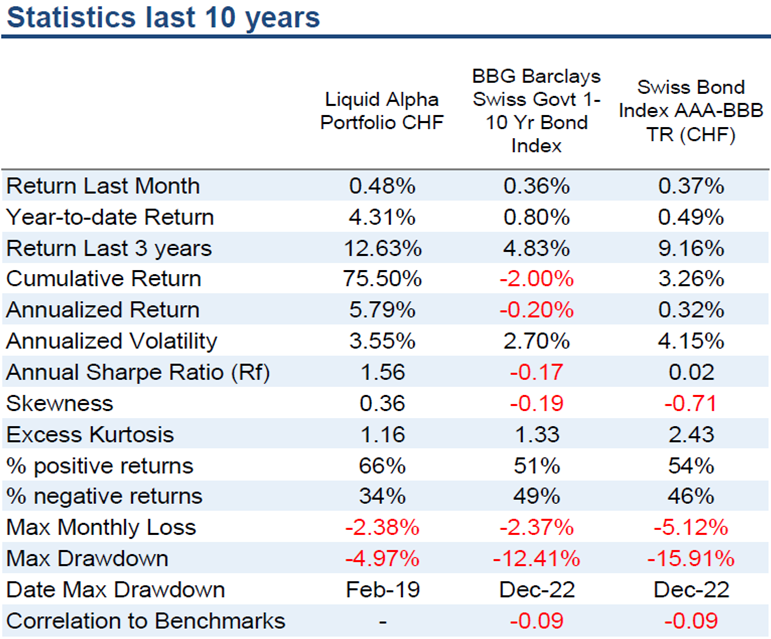

The following statistics over the last 10 years clearly demonstrate this: An annualized return of +5.8% compared to -0.2% for Swiss government bonds and +0.3% for investment grade bonds in CHF. The risk of bond investments at 0% interest is also clearly reflected in the loss of -12.4% and -15.9% respectively when interest rates rose in 2022.

It would be a shame if the same mistake were to be made twice with a short time lag. There are a number of better options than CHF bonds in this environment. Liquid hedge funds that pursue alpha strategies are one of them and will deliver an attractive return above the risk-free interest rate!

For a more detail discussion or more information by e-mail, please contact ss@cb-partners.com.

Zurück zu den negativen Zinsen in CHF

Ganze drei Jahre nach dem Zinsschock von 2022 hat die Schweizerische Nationalbank SNB den Leitzins wieder auf 0% gesenkt und die Marktzinsen am kurzen Ende sind bereits wieder negativ. Damit ist man zurück im Umfeld von 2014 – 2021 als die Zinskurve für CHF Obligationen grösstenteils negativ war. Damals wie heute gilt, dass es keinen Sinn macht, Risiken einzugehen, wenn man keine Rendite erzielen kann. 2022 hat zudem deutlich vor Augen geführt, wie schmerzhaft Obligationenanlagen sein können, wenn die Zinsen plötzlich steigen.

Die Risiken sind heute nicht kleiner als damals. Neben einer weiteren Inflationswelle wegen der US Zollpolitik und Deglobalisierung, spitzt sich auch die weltweite Schuldenkrise weiter zu, die eine höhere Verzinsung erzwingen wird. Die Zentralbank der USA ist nicht grundlos sehr zurückhaltend bei ihren Zinssenkungen, um nicht plötzlich zum Gegenteil gezwungen zu werden.

Alternativen zu Obligationen, wie Immobilien, Infrastruktur und Private Debt sind alle illiquid. Zudem sind die Renditeerwartungen eher bescheiden, wenn man berücksichtigt, dass man sich für 10 Jahre und mehr verpflichtet.

Aus unserer Sicht ist die beste Rendite/Risiko-Option ein liquides Alpha-orientiertes Hedge Fund Portfolio. Ein gut diversifiziertes Portfolio über Regionen, Anlageklasse und Nischenstrategien, die untereinander nicht korrelieren, ist entscheidend für eine stetige und stabile Rendite.

Unser Portfolio hat über 10 Jahre seit 2015 in CHF gut +5% pro Jahr netto aller Gebühren erreicht, während die Zinsen fast durchgehend negativ waren. Da alle Anlagestrategien weitgehend marktneutral und die Manager ausgewiesene Spezialisten in ihren Nischen sind - mit langen, erstklassigen Track Records, die viele Krisen überwunden haben - ist ein ähnliches Resultat auch über die nächsten 10 Jahre mit sehr hoher Wahrscheinlichkeit zu erreichen. +5% pro Jahr oder 0% pro Jahr machen über 10 Jahre einen riesigen Unterschied aus, der vielen Pensionären das Leben erleichtern würde.

Der Chart oben zeigt, das sich das Liquid Alpha Portfolio in CHF unabhängig vom Marktumfeld stets positiv entwickelt hat, während man weder mit Schweizer Bundesobligationen noch mit Unternehmensanleihen guter Bonität in CHF etwas verdienen konnte.

Die nachfolgende Statistik über die letzten 10 Jahre führt es deutlich vor Augen: Eine annualisierte Rendite von +5.8% gegenüber –0.2% bei Bundesobli und +0.3% bei Investment Grade Bonds in CHF. Auch das Risiko von Obligationen-Anlagen bei 0% Zins kommt durch den erlebten Verlust von –12.4% respektive –15.9% beim Zinsanstieg im 2022 deutlich zum Ausdruck.

Es wäre schade, wenn der gleiche Fehler zweimal innert kurzem Zeitabstand gemacht werden würde. Es gibt in diesem Umfeld eine Reihe besserer Optionen als CHF Obligationen. Liquide Hedge Funds, die Alpha Strategien verfolgen, gehören dazu und liefern eine attraktive Rendite über dem risikofreien Zinssatz!

Für weitere Informationen, schreiben Sie an ss@cb-partners.com.